Skip to content

Skip to content Intrinsic Value Assessment of ZIM Integrated Shipping Services Ltd. (ZIM)

By Christoph Wolf From The Investor’s Podcast Network | 04 April 2023

INTRODUCTION

ZIM Integrated Shipping Services Ltd. (ZIM), which dates back to 1945, is an Israel-based global container liner shipping company operating in more than 90 countries serving approximately 34,000 customers in over 300 ports worldwide.

The company uses digital strategies and a commitment to ESG values to provide customers innovative seaborne transportation and logistics services and outstanding customer experience.

One of its competitive advantages lies in its focus on major trade routes in selected markets, where the company possesses a strong position.

Another niche is ZIM’s unique approach to mostly charter instead of own most of its vessels, which allows the company to operate on an asset-light approach. On the other hand, this makes ZIM more dependent on the development of freight rates, which adds to uncertainty.

ZIM’s stock has been extremely volatile. During the last 2 years it went from $12 to $72 and now stands at $24. While this stock behavior surely reflects the uncertainty of the business, one must also consider the enormous dividend paid. In 2022 alone, $16.95 per share were distributed via dividends— which equates to a dividend yield of about 70% based on the current stock price. Considering a P/B of 0.5 and a P/E of 0.64, this valuation just looks absurdly cheap.

The reason for this extremely depressed valuation lies in the uncertainty of the near future. The forecast for 2023 is only $1.8-2.2 billion adjusted EBITDA and $100-500 million adjusted EBIT – which is vastly lower than the corresponding values in 2022 of $7.5 billion and $6.1 billion, respectively.

Is ZIM a dream come true for any value investor or will the strong headwinds in the near future turn this dream into a nightmare?

INTRINSIC VALUE OF ZIM

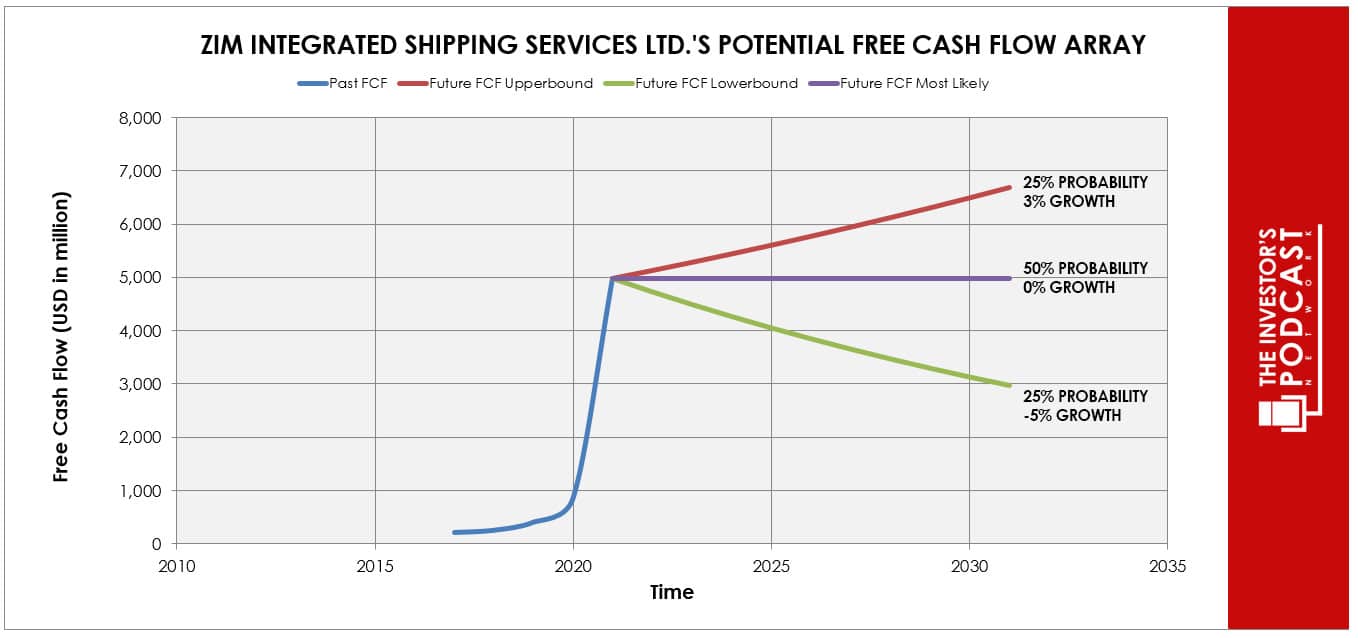

When determining the intrinsic value of a company, the general approach is to use the company’s history of free cash flows. Unfortunately, this only yields limited insight into ZIM. To see why, let’s have a look at the following plot of historical free cash flows:

As one can see, it is very hard to predict the company’s prospects based on this chart. Firstly, the data is limited to only 5 years. Secondly, 2021 seems to be an outlier and we cannot expect to see comparably high free cash flows in the near future.

Assuming for example a 25% probability for the upper growth rate of 3% per year, a baseline scenario of zero growth with a 50% probability and a worst case of a decline of 5% annually (with a 25% probability), the expected annual return is 171%. This is obviously not realistic.

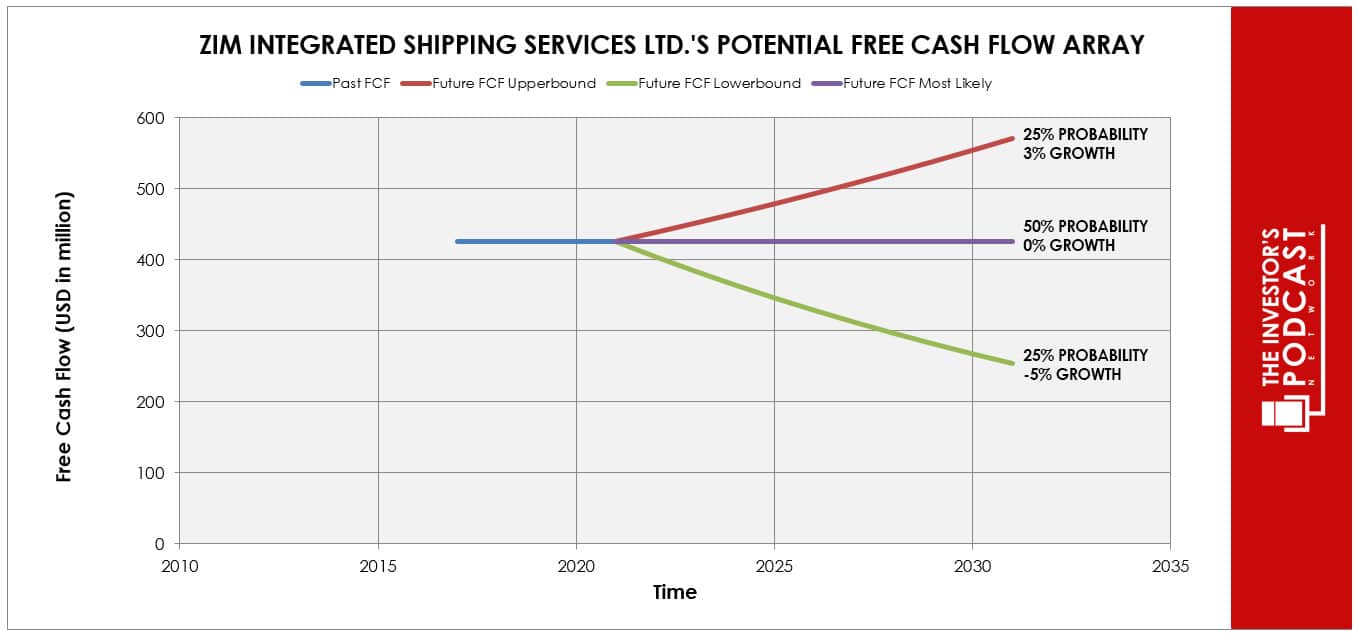

While it comes with vast uncertainty, we instead aim to estimate the expected annual return as follows: Firstly, we consider the FCF value of $4977 million in 2021 as a one-off event and do not take it into consideration for the estimate. Next, we take the average FCF values of the previous 4 years – the longest period for which data exists —which gives us an average FCF value of $425 million. Using this as a starting point, we again assume the same probabilities and values for the best, baseline and worst case as above.

This approach results in an expected annual return of 13.9%.

Since the prediction of ZIM’s future earnings or cash flows is very unreliable due to the high volatility of the company’s financials, we should at least make sure that the company stands on a solid foundation and has only limited debt.

An examination of the balance sheet reveals that ZIM stands on a sound financial footing. Its current ratio and quick ratio are both healthy with values of 1.60 and 1.52, respectively. While the debt/equity ratio is 0.5, all of ZIM’s long-term debt consists of long-term lease-liabilities. While this is still regular debt, it simply cannot be avoided by a company that charters most of its fleet. In this regard, management looks competent and does not load up on unnecessary debt.

In summary, ZIM looks very cheap. Still, one should keep in mind that due to the limited amount of historical data and the large volatility in the financial results, any forecast is prone to vast uncertainty.

THE COMPETITIVE ADVANTAGE OF ZIM

ZIM possesses some unique advantages that should allow it to be successful in the future:

- Asset-Light Business model. At the end of 2022, ZIM operated a fleet of 150 vessels, of which 94% were chartered. For comparison, the corresponding value of its competitors was only 45% on average. This allows the company to run the business with much less assets and capital.

- Differentiated global niche-strategy. ZIM operates on a global scale (more than 300 ports in 90+ countries) with a strong focus on major trade routes in selected markets, where it holds a competitive advantage.

- Strong Balance Sheet. Its debt/equity ratio stands at 0.5 and the current and quick ratio are 1.60 and 1.52, respectively. A solid financial footing is especially important when a business is so volatile.

When looking at various investing opportunities in the market today, let’s compare the expected return of ZIM to other ideas. First, one could invest in the ten-year treasury bond which is producing a 3.37 % return. Considering the bond is completely impacted by inflation, the real return of this option is likely negative. Currently, the S&P 500 Shiller P/E ratio is 28.3. As a result, the US Stock market is priced at a 3.5% yield. If one were to invest in the S&P 500, they might purchase a low-cost ETF to take advantage of this return.

MACRO FACTORS

The container shipping industry is volatile and highly unpredictable.

Especially in recent years this uncertainty has increased due to the US-China related trade restrictions, the retreat of free trade, the COVID-19 pandemic, the Russian invasion of Ukraine, and other factors. This makes running a business in this field especially hard, since even the near-term outlook is almost impossible to predict.

ZIM tries to counter this uncertainty at least partially by keeping a solid balance sheet and using its asset-light business model to focus on major trade routes in selected markets.

RISK FACTORS

There are several risks that might limit the growth prospects of ZIM:

- Volatile business. The container shipping industry is extremely volatile and depends strongly on the state of the world economy and of the existence of free trade. Due to the US-China tensions, the COVID-19 pandemic, rising inflation and interest rates, and many more factors, the near and midterm outlook look very fragile.

- Variable freight rates. Since ZIM charters most of its fleet, the company is very sensitive to fluctuations in the charter market. As the costs associated with chartering vessels are unpredictable, this adds to uncertainty.

- Intense competition. ZIM has multiple competitors and some of these – such as Moller-Maersk and MSC – are huge companies running vast fleets. It can be hard for ZIM to compete with these large firms due to their immense clouts and economies of scale.

SUMMARY

ZIM is an intriguing investment idea. On the on hand, the company looks absurdly cheap, has a solid balance sheet, and has paid an extremely high dividend. The reason for this depressed valuation lies in the vast uncertainty and volatility of the business the company is operating in. While the expected annual return of 13.9% looks appealing, one should remember that this estimate is based on rather shaky foundations. Before investing in this stock, investors should surely dive deeper into the company’s risk profile.

To learn more about intrinsic value, check out our comprehensive guide to calculating the intrinsic value of stocks.

Disclaimer: The author does not hold ownership in any of the companies mentioned at the time of writing this article.