Skip to content

Skip to content Intrinsic Value Assessment Of Network-1 Technologies Inc. (NTIP)

By David J. Flood From The Investor’s Podcast Network | 12 March 2018

INTRODUCTION

Network-1 Technologies Inc. is a U.S. based communications equipment company whose principal business involves the development, licensing, and protection of intellectual property. At the time of writing, the firm’s market cap stands at around $59 Million and its revenues and free cash flows for the previous financial year were around $16 Million and $6 Million respectively. The company’s common stock has fluctuated between a high of $3.25 and a low of $2.00 over the past 52 weeks and currently stands at $2.48. Is Network-1 Technologies Inc. undervalued at the current price?

THE INTRINSIC VALUE OF NETWORK-1 TECHNOLOGIES INC.

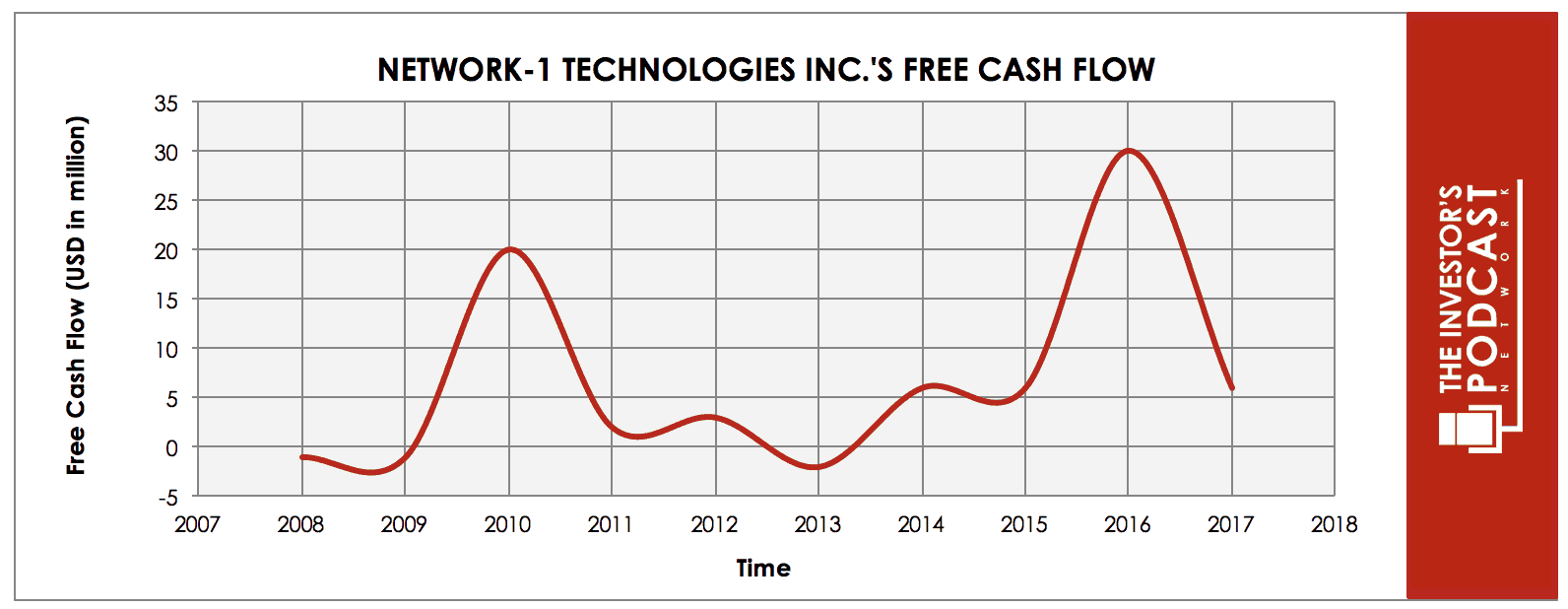

To determine the intrinsic value of Network-1 Technologies Inc., we’ll begin by looking at the company’s history of free cash flow. A company’s free cash flow is the true earnings which management can either reinvest for growth or distribute back to shareholders in the form of dividends and share buybacks. Below is a chart of Network-1 Technologies Inc.’s free cash flow for the past ten years.

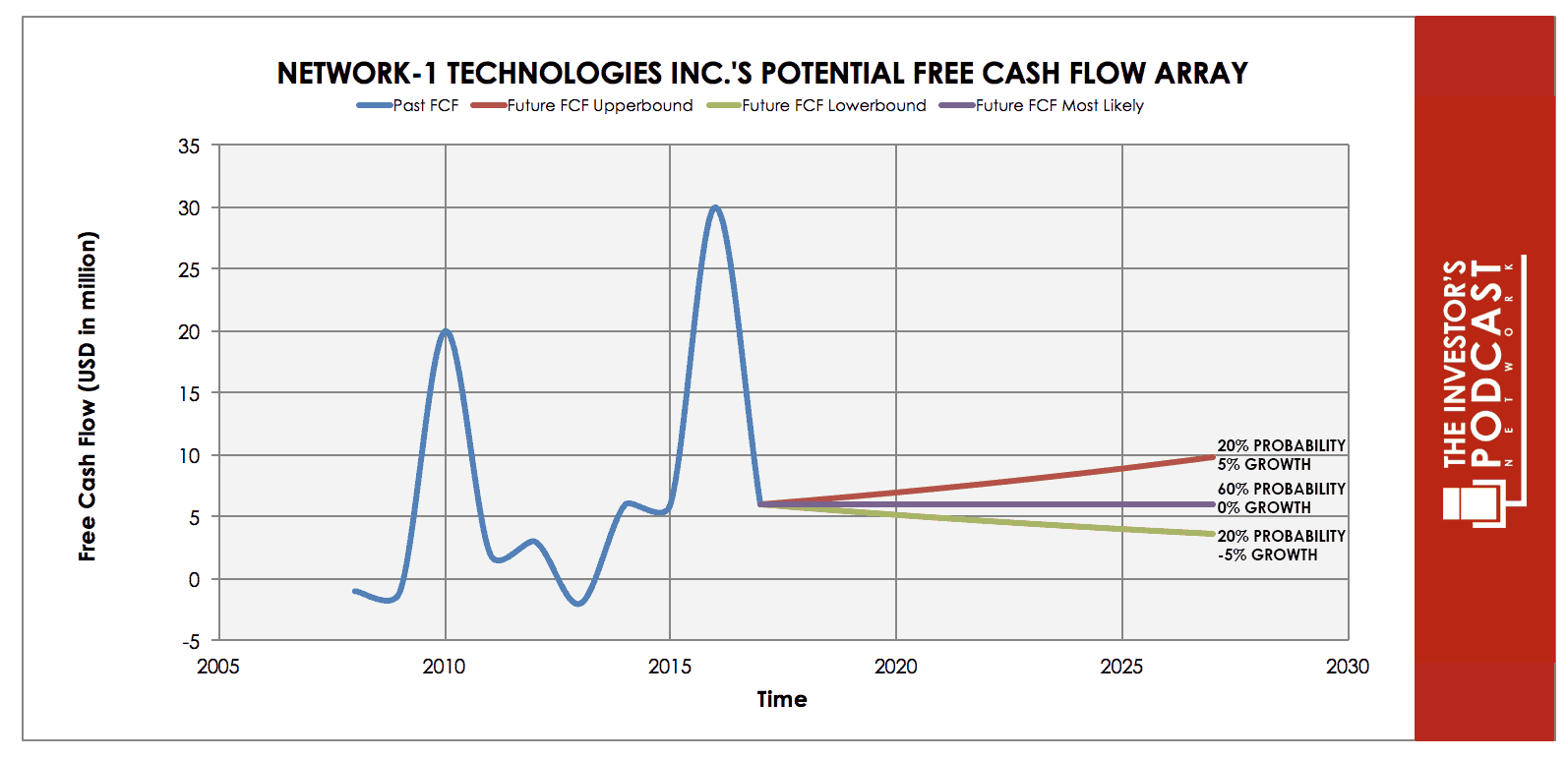

As can be seen, the firm’s free cash flow has fluctuated significantly over the past decade. This is a result of the fact that the company receives money to license its patents in either lump sums or through ongoing royalty payments. The firm must also enforce its patent protection through legal proceedings which can result in delays in payments. In order to determine Network-1 Technologies Inc.’s intrinsic value, an estimate must be made of its potential future free cash flows. To build this estimate, there is an array of potential outcomes for future free cash flows in the graph below.

When examining the array of lines moving into the future, each one represents a certain probability of occurrence. The upper-bound line represents a 5% growth rate which assumes that the firm’s future free cash flow growth is driving by additional patent acquisitions and through the firm’s recently investment the clinical stage biotech company, ILiAD Biotechnologies. This upper growth line has been assigned a 20% probability of occurrence to account for the uncertainties associated with securing future profits from subsequent patents and investments.

The middle growth line represents a 0% growth rate which assumes future free cash flow does not increase. This scenario assumes that the firm does not successfully win ongoing legal proceedings and that its recent patent additions and investments do not progress favorably. This growth rate has been assigned a 60% probability of occurrence to account for the uncertainty which currently surrounds the company.

The lower bound line represents a -5% rate in free cash flow growth and assumes that the company suffers a period of contraction in earnings due to future patent expirations. This growth rate has been assigned a 20% probability of occurrence.

Assuming these potential outcomes and corresponding cash flows are accurately represented, Network-1 Technologies Inc. might be priced at an 8.4% annual return if the company can be purchased at today’s price. We’ll now look at some other valuation metrics to see if they correspond with this estimate.

Network-1 Technologies ’s current free cash flow yield, which is the inverse of its Price/FCF ratio, is 15.25%. This is based on a ttm free cash flow of $9 Mil, assuming a $6 Mil free cash flow, which the firm achieved in three of the last four years, would result in a 10.16% free cash flow yield.

Finally, we’ll look at Network-1 Technologies Inc.’s book value growth and dividend yield to see whether this supports our other estimates of growth. Year-on-Year book value has grown at an annualized rate of around 6%, and the current dividend yield stands at around 4%. Assuming Network-1 Technologies can grow its book value at a similar rate for the next ten years and its current dividend yield can at least be maintained, the firm should return around 10% at the current price.

Taking all these points into consideration, it seems reasonable to assume that Network-1 Technologies Inc. may return between 8-10% at the current price if the estimated free cash flows are achieved. Now, let’s discuss how and why these estimated free cash flows could be achieved.

THE COMPETITIVE ADVANTAGE OF NETWORK-1 TECHNOLOGIES INC.

Network-1 Technologies Inc. has various competitive advantages outlined below.

- Intangible Assets. Network-1 Technologies currently holds a portfolio of 28 patents which protect its proprietary technology. These intangible assets are the primary source of earnings for the company, and it aggressively protects them through legal action.

- The Remote Power Patent covering the delivery of power over Ethernet (PoE) cables for the purpose of remotely powering network devices, such as wireless access ports, IP phones, and network-based cameras;

- The Mirror Worlds patent portfolio (the “Mirror Worlds Patent Portfolio”) relating to foundational technologies that enable unified search and indexing, displaying and archiving of documents in a computer system;

- The Cox patent portfolio in relating to enabling technology for identifying media content on the Internet and taking further action to be performed based on such identification; and

- Patents covering systems and methods for the transmission of audio, video, and data over computer and telephony networks in order to achieve a high quality of service (QoS) (the “Qos Patents”).

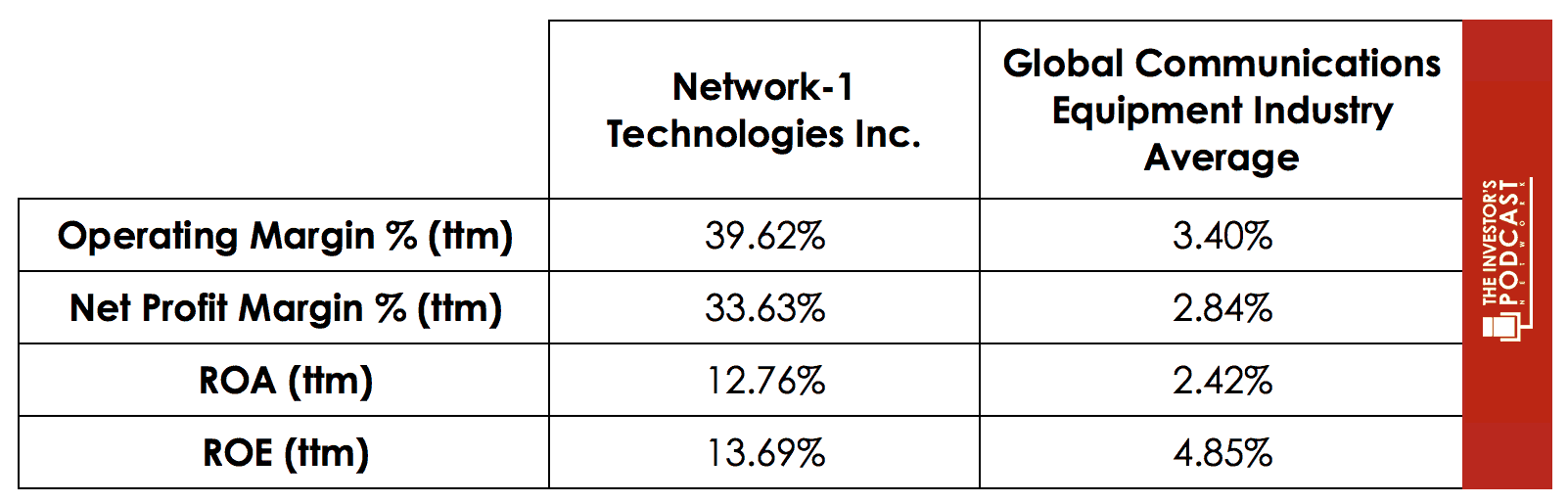

- Low-cost Operations. Since Network-1 Technologies Inc. is an intellectual property company which generates earnings from the acquisition, licensing, and enforcement of patents it only requires a small workforce of under ten These low-cost operations allow the firm to achieve performance metrics well more than the Global Communications Equipment Industry averages.

- Strong Corporate Culture. Network-1 Technologies Inc’s management is closely aligned with shareholders with insider ownership currently standing at around 26%. The firm has also begun to pay dividends in recent years and has bought back around $15 Mil in shares since 2011. Considering the large levels of cash and equivalents on the balance sheet and the prospect of favorable outcomes in ongoing legal proceedings, the chance exists that these dividends may increase, or a special dividend may be paid.

NETWORK-1 TECHNOLOGIES INC.’S RISKS

Now that Network-1 Technologies Inc.’s competitive advantages have been considered, let’s look at some of the risk factors that could impair my assumptions of investment return.

- Network-1 Technologies Inc. currently has multiple legal proceedings in play including those against Hewlett Packard and Google. If these legal proceedings are not resolved in a favorable manner, then the firm stands to not only lose out on $100-200 Mil in potential damages but will be unable to collect royalties from other companies who are withholding payments while legal proceedings are ongoing.

- Network-1 Technologies Inc.’s business is dependent on the acquisition and monetization of patents. A number of the patents which have accounted for a significant portion of the firm’s past earnings are set to expire within the next few years. If the company is unable to acquire and successfully monetize new patents, its economic future is likely to be negatively impacted.

- Network-1 Technologies Inc. has recently invested in the clinical stage biotechnology company, ILiAD There is always an element of risk with the probability of success for clinical trials, and there is no guarantee that this investment will prove a useful allocation of capital for the firm.

OPPORTUNITY COSTS

Whenever an investment is considered, one must compare it to any alternatives to weigh up the opportunity cost. At the time of writing, 10-year treasuries are yielding 2.63%. If we take inflation into account, the real return is likely to be closer to 1%. The S&P 500 Index is currently trading at a Shiller P/E of 29.4 which is 74% higher than the historical mean of 16.9. Assuming reversion to the mean occurs, the implied future annual return is likely to be -1.6%. Network-1 Technologies Inc., therefore, appears to offer a much better return for investors at present, but other individual stocks may be found which offer a similar return relative to the risk profile.

MACRO FACTORS

Investors must consider macro-economic factors that may impact economic and market performance as this could influence investment returns. At present, the S&P is priced at a Shiller P/E of 29.4. This is 74% higher than the historical average of 16.9 suggesting markets are at elevated levels. U.S. unemployment figures are at a 48-year low suggesting that the current business cycle is nearing its peak. U.S. private debt/GDP currently stands at 202.80% and is at its highest point since 2009 when the last financial crisis prompted private sector deleveraging.

SUMMARY

Network-1 technologies Inc. is currently selling at a discount to fair value due to negative market perception relating to the uncertainties surrounding court proceedings, cash settlements, and withheld royalties’ payments from other licensees. Investors should be aware that there is no guarantee that the company will be successful in its claims of patent infringement against Hewlett Package, Google, and other companies.

Network-1 Technologies Inc. does, however, have a very good track record in winning legal battles based upon patent infringement. The company’s most recent 10-Q notes that;

“In September 2011, we initiated patent litigation against sixteen (16) data equipment manufacturers in the United States District Court for the Eastern District of Texas, Tyler Division, for infringement of our Remote Power Patent. We settled the litigation against fifteen (15) of the sixteen (16) defendants. The remaining defendant in the litigation is Hewlett-Packard Company.”

Given that the company has a strong track record of winning legal battles against companies such as Sony, Motorola, Samsung, and Huawei, it seems reasonable to assume that Network-1 Technologies may be successful in one or more of its current patent infringement cases. If the Hewlett Packard case can be successfully won then, the firm will not only receive a significant sum from the ruling but will also be able to rightly lay claim to unpaid royalties’ payments from Cisco, Dell, and Netgear.

The company is currently in a very strong financial position with no debt to speak of and a formidable liquidity position as evidenced by the firm’s quick ratio of 26.72. As of the most recent quarter, around 93% of the company’s balance sheet is comprised of cash and equivalents. Given that the firm is currently trading at around 1x, book value investors have the potential to make an investment which offers the potential for significant upside with excellent downside protection.

The projected return of 8-10% is based on extremely conservative assumptions for the company and does not take into account the possibility for significant upside if the legal challenges are successful.

In summary, Network-1 Technologies Inc. in an investment with significant upside potential and credible downside protection. Investors must be prepared for continuing uncertainty and patience will be required to see this investment play out. Based on the conservative assumptions used in the analysis of the company, Network-1 Technologies Inc. may return around 8-10% at the current market price. If the firm is successful in the current legal battles it is engaged in, this upside could be much higher.

To learn more about intrinsic value, check out our comprehensive guide to calculating the intrinsic value of stocks.

Disclosure: The author holds fractional ownership in Network-1 Technologies Inc.