Skip to content

Skip to content

Stig Brodersen’s Track Record Since 2014

By Stig Brodersen • 11 min read

Dear listeners of The Investor’s Podcast,

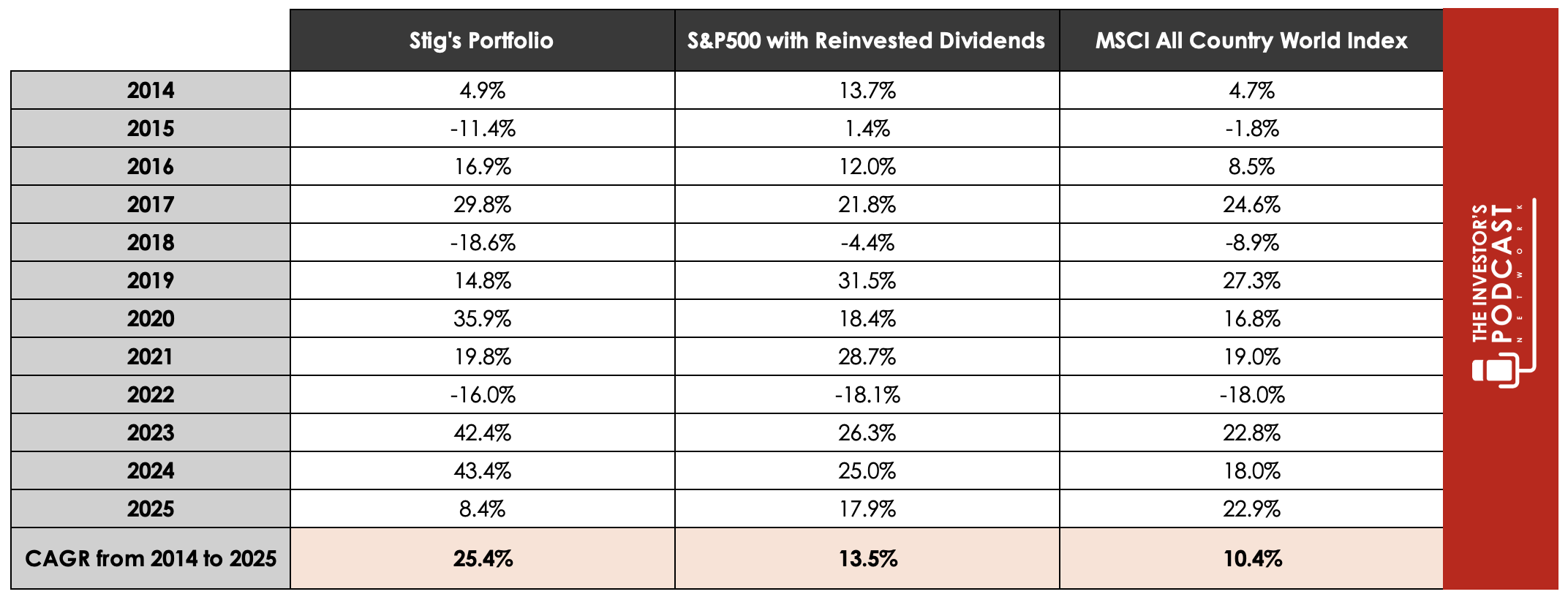

2026 was a disappointing year. My portfolio had a 8.4% return vs. 17.9% for the S&P 500 and 22.9% for the MSCI All Country World index. In my previous letter, I noted that continuously outperforming the benchmarks would be the exception rather than the rule. Unfortunately, I can now confirm that this statement was both accurate and timely.

New Additions

I consider a year with just one good investment idea to be a terrific year. Whether that proves true in hindsight remains to be seen, but in 2025, I found only one: Uber. I built the position in three tranches, starting on 23 September, and by year-end, it represented 6.7% of my public portfolio at an average purchase price of $95.45.

Uber has been on a tear in 2025. Shrewd investors who bought at the bottom and sold at the top would have made roughly 70%. Yours truly managed to lose 14.5% at year’s end, and as so often before, demonstrated a masterclass in what not to do.

To beat the stock market, there are generally three levers you can pull. The first is having better information than the market, which typically falls into two categories. One is insider information, which is illegal. The other is scuttlebutt-style research, which tends to be more effective for smaller companies. At a market capitalization of $180B, Uber is not a small company—and I certainly don’t have any insider information.

The second lever you can pull to beat the market is to have a better temperament than other investors. This is a tricky topic to discuss. I know roughly as many investors who believe they have an above-average temperament to win in the stock market as I know people who think they are below-average drivers (roughly 0). Fun fact: A study found that drivers who were hospitalized after an accident they acknowledged causing still believed they were above-average drivers!

Therefore, simply asking people whether they think they have better than average temperament is about as useless as you would think. A decade of outperformance through at least one painful bear market is a meaningful signal of investor temperament. Multiple decades and multiple bear markets leave far less room for doubt.

Finally, the third lever is superior analysis of market information. If I’m right about my Uber investment, this is the lever I’m betting on. The market still seems anchored to a narrative that Uber is being disrupted by autonomous vehicles. I see it differently. I believe autonomous vehicles will be a meaningful tailwind rather than a threat. Moreover, I don’t think ride-hailing, traditionally how people think about Uber, will be the company’s most important business in ten years. Instead, I expect delivery, which is far harder to automate, to move front and center.

When I look at Uber, I see a company growing at roughly 20% annually, with a long runway ahead, significant operational leverage, and a large advertising business under the hood that the market appears to underappreciate.

It’s true that Uber, like many companies today, pays too much in share-based compensation. Offsetting dilution through buybacks is not free; it’s real capital that could otherwise be paid out as dividends or reinvested in the business. That said, Uber’s sizable buyback program has recently reduced the company’s outstanding share count, with no signs of slowing business growth. While this is far from perfect capital allocation, at the current price level, I believe it sets up the potential for attractive returns over the coming decade.

Divestiture

A friend of mine is an executive at a public company and told me the other day, “Everyone tells you that they are long-term investors until the stock price goes down.” From more than a decade in the financial markets and speaking with thousands of investors, I’m inclined to agree with him, and I might be as guilty as charged.

I sold one company in 2025: Evolution AB, a gaming software provider. Looking at the scoreboard, I exited with a -10.0% return. I’m a contrarian by nature, and it’s one of the reasons why the value investing community appeals so much to me. To be successful in the stock market, you have to be willing to go against the crowd and make your own decisions when everyone tells you that you are wrong.

That said, the opposite of a virtue is also a virtue. And as I learned in 2025, as I have so many times in the past (when do I learn?), is that more often than not, when a stock drops, there are typically good reasons for it, and what might look cheap is often a falling knife. Evolution AB is no different. Of course, when I invested in the stock, I knew that the company had various issues and slowing growth, but that doesn’t disqualify a stock in my book. When I built my position, I was getting an 8% shareholder yield, roughly split between dividends and buybacks, and I had modelled the growth in the low double digits, bringing the total return closer to 20% annually in the bull case.

However, this time around the world wasn’t that kind. Evolution AB encountered problems worse than I had expected. I sometimes tend to forget that the best companies always surprise you with more good news, whereas not-so-great companies would often continue to surprise you with the opposite.

Ultimately, investing is a game of probabilities. While I’m by no means proud of my investment in Evolution, I’m thinking about everything in my portfolio (and life) as probabilities. There was never a 100% probability that any specific scenario would play out for the company. It was all on a spectrum, and if we played out the situation 1,000 times, we would undoubtedly have found situations that were both much better and much worse than what actually happened.

As investors, all we can do is place our bets where our analysis shows that the odds are in our favor and diversify appropriately to let the math work in our favor and limit our downside. A track record is the result of all of your bets.

CAGR = Compounded Annual Growth Rate

- The S&P500 data can be found here and does not use a dollar-weighted approach.

- The MSCI All Country World Index data can be found here and does not use a dollar-weighted approach.

- My returns have been calculated by Sharesight using the dollar-weighted approach and can be found here.

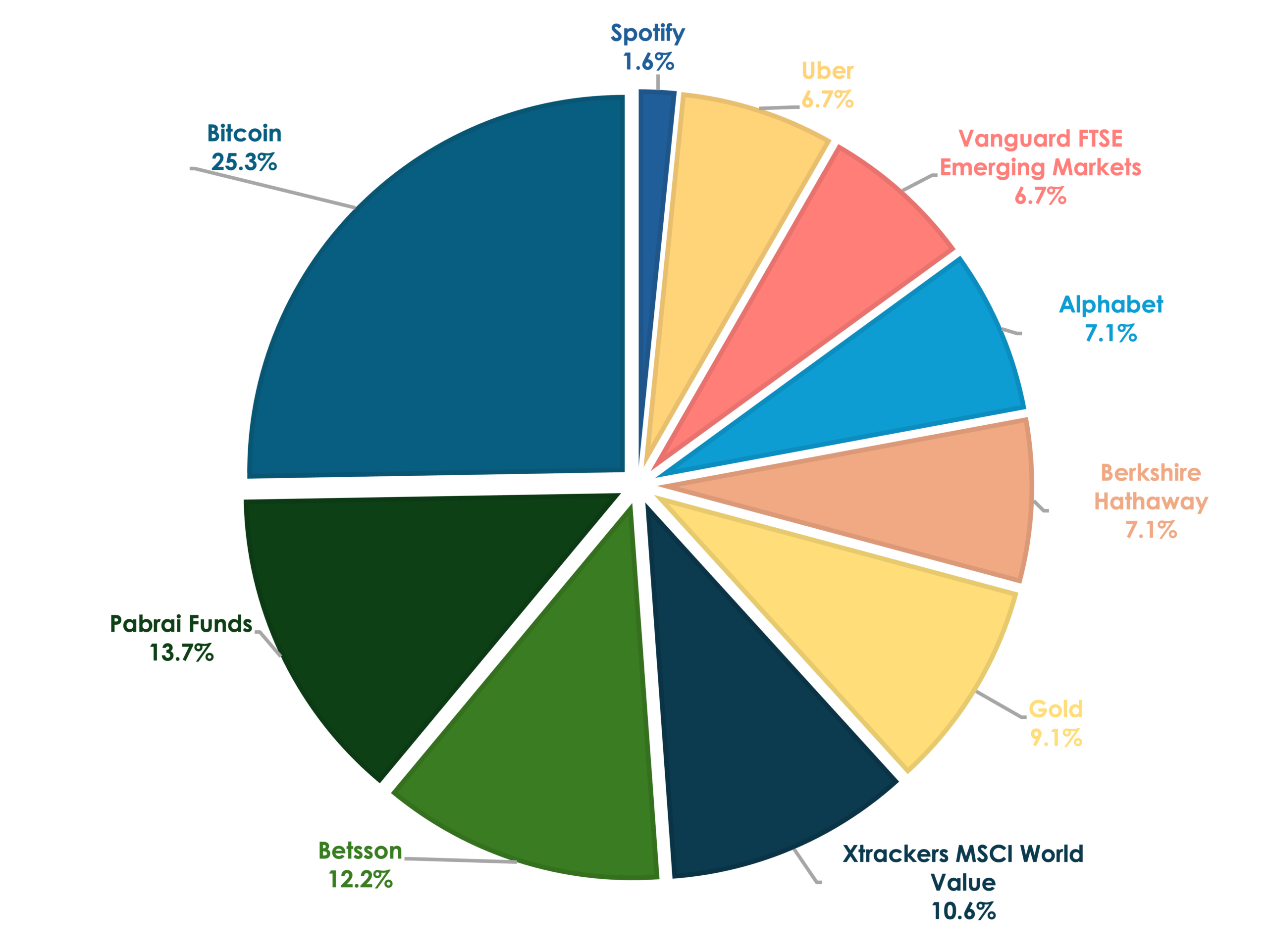

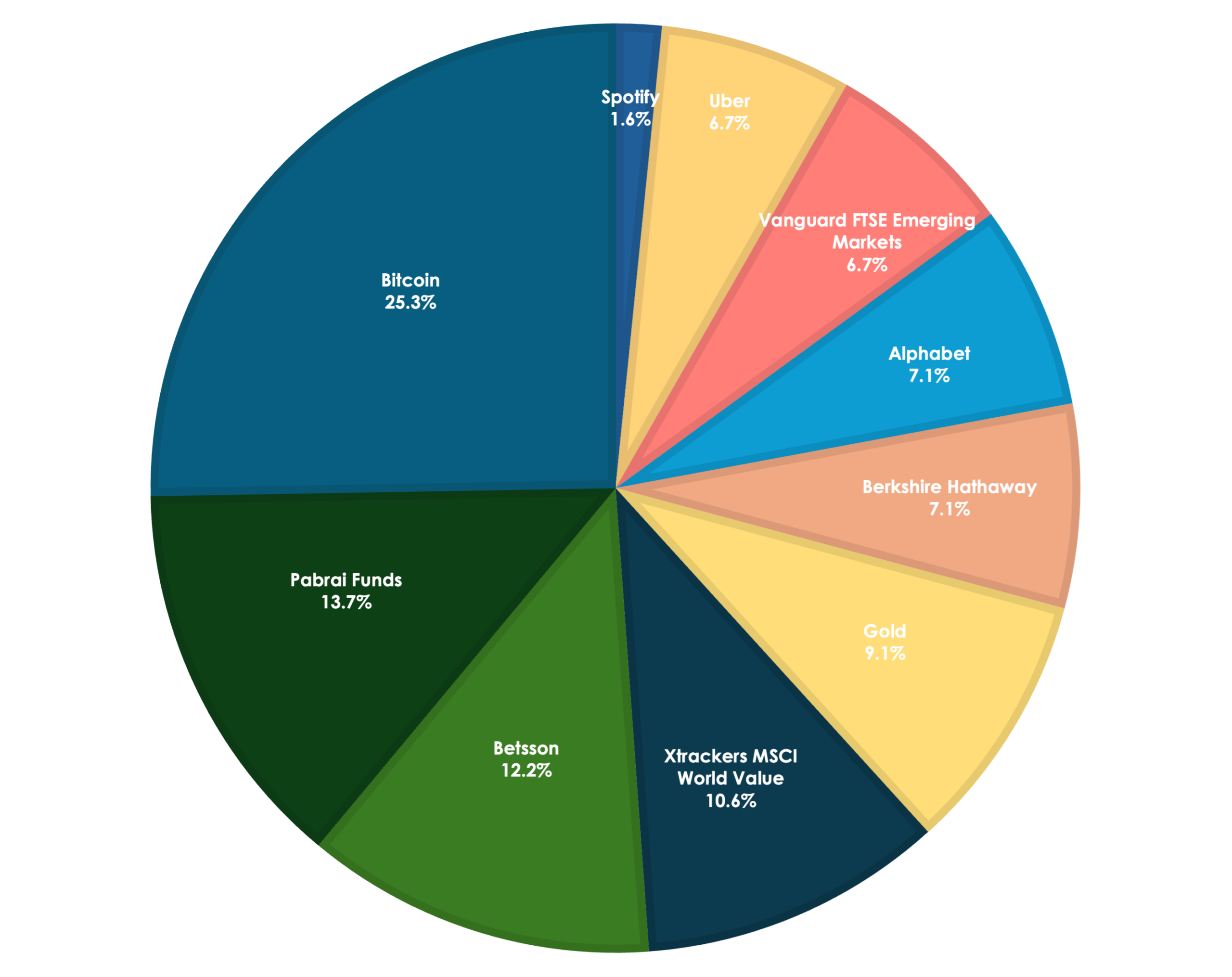

STIG BRODERSEN’S PORTFOLIO AS OF 31 DECEMBER 2025

Below, I have listed my current holdings. Since our founding in 2014, we have hosted a mastermind discussion roughly once a quarter where we document what we invest in and what is on our watchlist. If you’re curious about the bull theses on my positions, I’ve linked them to the corresponding mastermind discussion or other relevant episodes.

Bitcoin | Pabrai Funds | Betsson | Berkshire Hathaway | Xtracker World Value

Vanguard FTSE Emerging Markets | Physical Gold | Uber | Alphabet | Spotify

Holding Period: A Consequence, Not a Goal

For a portfolio I started in public in 2014, I was a little surprised to see that the holding period is 5.1 years (5.5 years money-weighted). That said, a longer holding period isn’t a goal in itself. Rather, the longer holding period is consistent with the portfolio’s goals as outlined in the 2024 letter, but it also reflects a degree of reflexivity. In other words, holding for a long period of time often, but not always, leads to better returns, which in turn nudges you to continue following a more passive buy-and-hold strategy.

At the end of the day, you want the best risk-adjusted returns that can meet your financial goals. This implies that you sometimes need to sell out of a position because the valuation gets ahead of itself, even if it’s a wonderful company, and it does sometimes pay to buy into a company if the price-to-value ratio is heavily skewed in your favor. One example is that I originally bought Spotify on 11 January 2020 at $186.30 and fully exited the position on 19 January 2021 at $318.80. I later bought back in on 5 December 2022 at $78.70,

Similarly, if you have private alternatives available to you, they introduce an additional layer of opportunity cost you can use to your advantage. While there is some correlation between expected returns in the private and public markets, public markets are far noisier, and networking can occasionally unlock unique, high-return private opportunities. A meaningful difference in your favor between time-weighted and money-weighted returns in public markets is often a healthy sign that capital is being allocated where it is most productive.

Viewed through this lens, public investing naturally becomes the base layer of a portfolio. It is the most liquid and least energy-intensive component. On top of that, private investments can be added. It also brings the discussion back to the central point of this section. A long holding period in public markets is a consequence, not the goal, of your value investing strategy, and, as an added benefit, it frees up time and energy to accumulate capital in the first place.

Warmly,

Stig Brodersen | 23 January 2026

Dear listeners of The Investor’s Podcast,

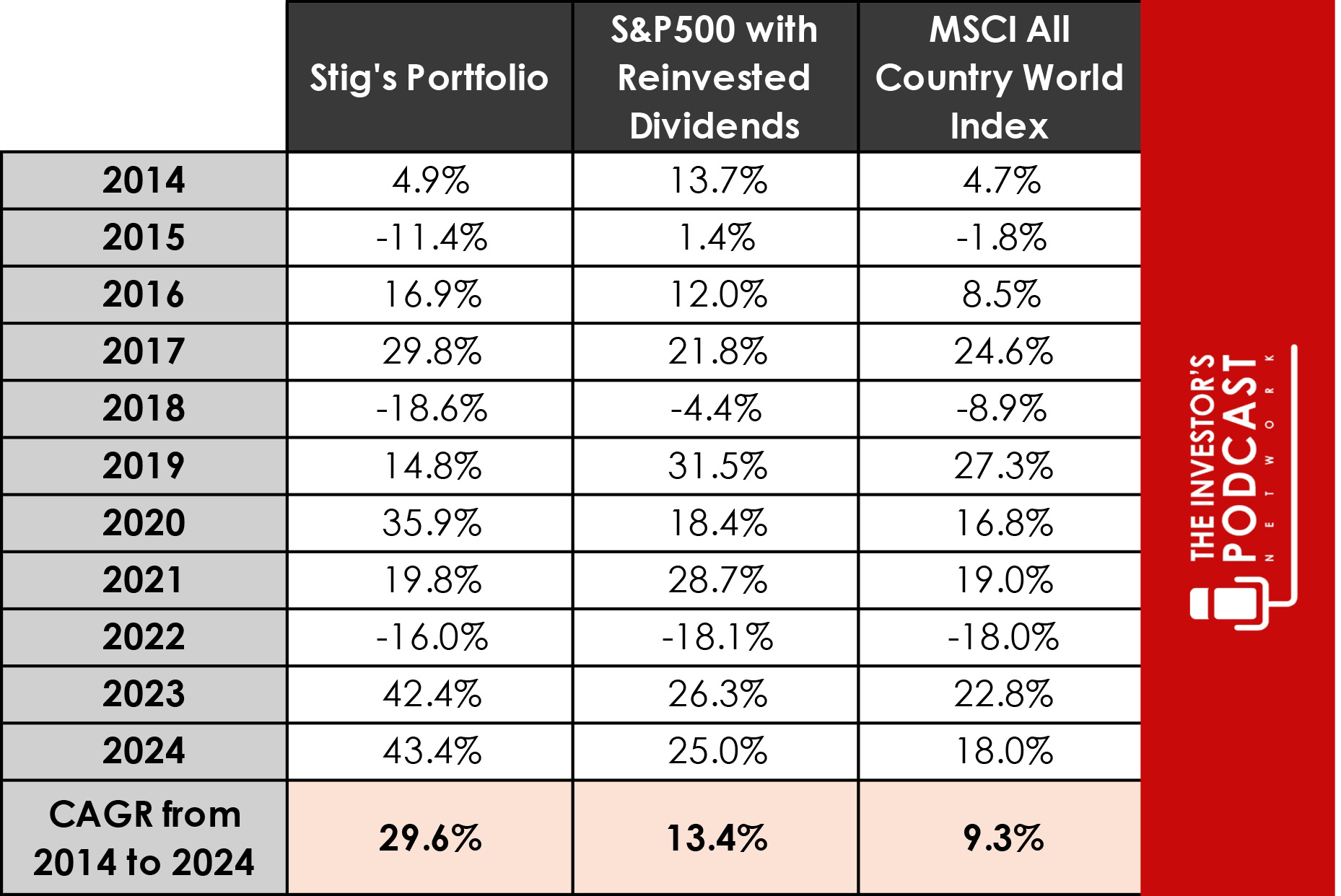

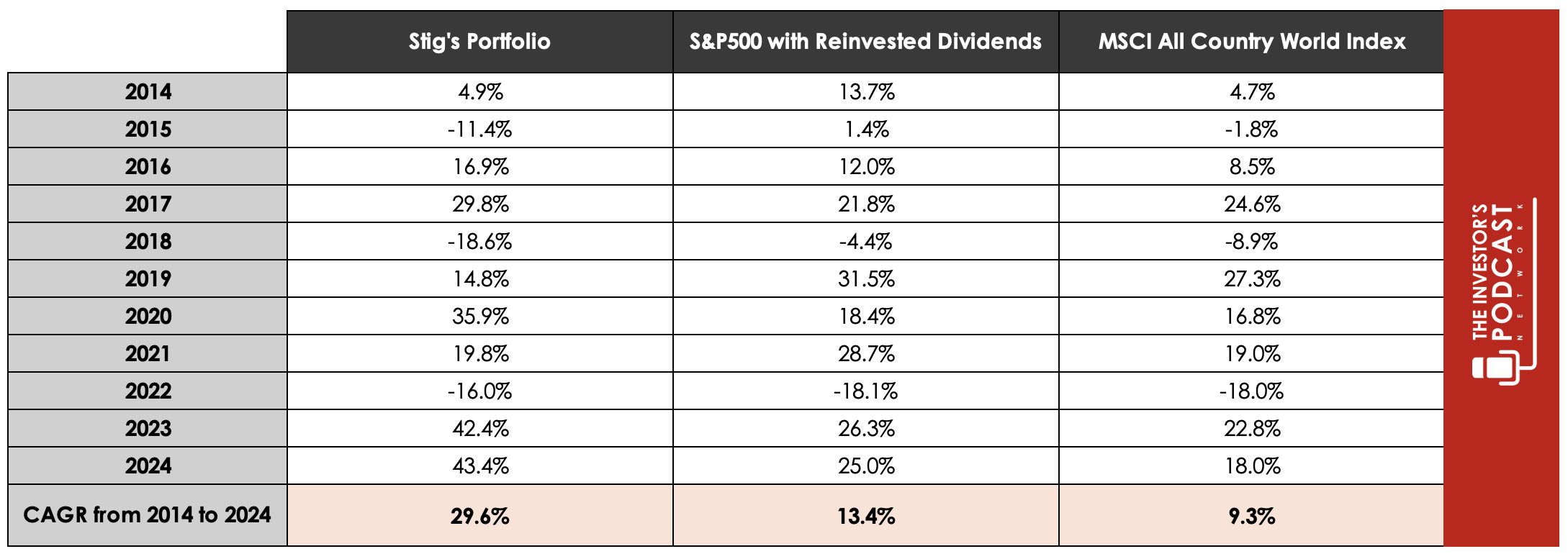

“Everyone looks like a genius in a bull market,” goes the old Wall Street aphorism. There is definitely something to it. In 2024, I made a 43.3% return vs. 25.0% for the S&P 500 and 18.0% for the MSCI All Country World index.

Luck played a major role. In future letters, you will see that this year is the exception and certainly not the rule. In 2023 and 2024, the S&P 500 returned more than 20% — when was the last time the S&P 500 did that for two consecutive years? We have to go back to 1997 and 1998. You might remember what happened next. If history is any guide, we should be in for quite a ride!

New Additions

2024 was an unusually busy year with two additions to the portfolio: Evolution Gaming Group and Betsson. After spotlighting these two names in quarterly Mastermind Discussions, my bullishness on them is no secret (for your convenience, I’ve linked to those episodes below.) Therefore, I won’t include too many details on the investment but encourage you to check them out in full via our free podcasts.

It’s no coincidence that both picks are in the gambling sector. To quote Willie Sutton when asked why he robbed banks: “Because that is where the money is!”If only life and investing were that simple. It is too early to tell if the new additions will work out, though early indications suggest the market tends to agree more with Betsson than with Evolution Gaming Group. I bought Betsson at an average price of SEK 118.7, and I’m receiving a generous dividend while waiting for the market to recognize the company’s quality.

After purchasing Evolution Gaming Group at an average price of SEK 1,010.6 in 2024, I’ve already added more shares this year at a further discount, bringing down the average price to SEK 956.1 for the entire position. Time will tell if I am averaging down into a value trap. It wouldn’t be the first time!

Evolution Gaming Group provides live casino software for the gaming industry. That is not quite as exciting as the early days of YouTube or Google Search. However, I do see a pattern in Evolution’s business resembling Alphabet’s prospects from several years ago, where there was a favorable shift in advertising growth amid a secular transition to digital advertising. I see similar structural tailwinds supporting the gambling industry, with Evolution Gaming Group benefiting from growth in gambling and live casinos, taking market share from traditional casinos.

In addition to Evolution Gaming Group and Betsson, I added to my positions in Vanguard FTSE Emerging Markets and Xtrackers MSCI World Value throughout the year.

Divestitures.

I exited two positions in 2024: Alibaba and Teqnion. In the value investing community, we pride ourselves on being contrarian and staying rational when others lose their heads. I am guilty as charged.

Having more than a decade of experience in the stock market and being deeply integrated into the value investing community, I’ve ironically found that we tend to behave like a herd, not so different from the other investing communities we enjoy criticizing. Like many value investors, I invested in Alibaba after Charlie Munger made his move. And, like so many other value investors, I prided myself on adding to my position as the stock price continued to slide while I was screaming at the top of my lungs how much of an independent thinker I was. But would I have made the plunge if Munger didn’t invest?

I lost well above 30% on my adventures in Alibaba, and much more when you consider my opportunity costs of investing during a bull market. It’s not the position where I’ve lost the most measured in percentages, though. Sadly, it’s not even close! But it’s the position where I lost the most dollars. I ended up closing my position at $74.3, took that money, and allocated it to Betsson. Time will tell if it was a good decision.

Looking at Teqnion, this was never more than a 1% position for me after buying in at an average price of SEK 201.6 and exiting at SEK 222.0 while owning the shares for slightly more than a year. I was in the fortunate position to become friends with the Deputy CEO, and it didn’t seem right to be invested and raise the suspicion that I would be able to trade on insider information.

The Goal of the Portfolio:

This is where I should put down a 10% or 15% target annual return on my portfolio. Truth be told, I did put down 15% before I decided to delete it. Why? I don’t see the portfolio’s goal as being just about a specific annual return.

- 1,000 / 1,000

My aim has been to achieve my financial goals as many times as possible across 1,000 different simulations, and I defined those goals, until recently, as being financially independent. Today, I’ve achieved that goal, and my focus is more on wealth preservation. I want to make sure that if I get hit by a bus tomorrow, my family will be taken care of for the rest of their lives, and as such, you can say that my goal is that the status quo doesn’t change (including the part about the bus!).

Financial independence for my family is: “Doing what you want to do for as long as you want with whoever you want.” As you look at my portfolio, this might sound ridiculous, given the concentration.

Peter Lynch famously said you “shouldn’t cut your flowers and water the weeds.” I couldn’t agree more. The portfolio you see below doesn’t reflect the original position sizings. My rule is not to invest more than 10% in any one position at cost, and I usually stick to it (there have been exceptions, but that is a story for another day). If I had to compose a portfolio at cost, it would look different and less concentrated. However, when investing in financial markets, we quickly learn that the market sends you different signals to pay attention to. If an investment takes off, it’s typically because your analysis has been right, and you should stay invested in your winners to reap the full benefits, hence watering the flowers and not the weeds.

One thing I often think about, and where I, by definition, do not have a good feedback loop, is how my portfolio would do 1,000 out of 1,000 times. If you look at Berkshire Hathaway today, I’m quite sure it won’t be the best performer over the next decade, but I’m almost certain it won’t be the worst. I want to have an anti-fragile portfolio. It’s for that reason that I have an allocation into hard money.

The world has become more uncertain than when I started investing, and my investments in gold and Bitcoin have, as a result, (sadly) performed better than I would have expected. If I ran my portfolio 1,000 times, facing an uncertain world, hard money would have a place in all of them, but the performance of hard money would have a wide distribution, and therein lies the entire point. When your goal is the status quo, you must protect yourself against inflation even more than usual.

I’m an avid student of financial history, perhaps to my own detriment. When something hasn’t happened in our lifetime, we tend to think it’s very unlikely to happen, and perhaps we don’t even think it’s possible. I factored in 0 pandemics when I built my portfolio. I had vaguely heard about the Spanish Flu, but in my mind, it was in the same category as the plague. Something that surely shouldn’t play any role in my lifetime. Now, the world is keenly aware of a pandemic, and we likely overestimate the probability of that happening again in the short term, in contrast to underestimating it (or completely disregarding it) as we did before 2020.

Reading history books, you discover that the world had never (effectively) been on a fiat standard before 1971. I don’t predict whether the US dollar will be the world reserve currency for the next XZY years, but I know that the last 54 years have been the exception to the rule. Most investors do not realize that fiat currencies tend to decline gradually and then suddenly. Depending on how long you zoom out, 54 years is a very long time or a blink of an eye.

Of the 750(ish) currencies that have existed since 1700, only roughly 20% remain, and of those that still exist today, all of them have been devalued significantly. Also, all reserve currencies throughout history have had their status usurped, typically through a painful process for at least one, and often multiple, of the reigning superpowers.

I don’t know what will happen. We live in a world with known unknowns and unknown unknowns. I want to reach my financial goals in as many, if not all, of 1,000 hypothetical scenarios.

- Optimize for happiness

I know I’m not supposed to check the quotes for my portfolio daily. Yet, I check them multiple times daily — and I love it! This might sound silly, but I’m quite sure I would still invest in individual stock picks even if I underperformed the market. Who picks stocks if you can’t beat the market? Well, I do! I do it for the same reason that I watch football. Even if nobody is paying me, I just love it!

Optimizing for happiness is also why I only own five stocks. I’m not opposed to owning 20 individual stocks, but I don’t think I could ever get there. I want to keep track of the companies in my portfolio and their competitors, and I have an ever-changing watchlist, too. If I had 20 stocks, I would feel stressed keeping track of everything and wouldn’t enjoy the process. I’m sure that others would be equally stressed by having the type of concentrated portfolio I have, but that is very much my point.

I would be surprised if someone owned 20 stocks in their portfolio for the same reason why I own five. Perhaps they can’t sleep if they don’t own 20+ stocks, which is not optimized for their happiness. Perhaps they run an investment fund and know they can’t grow the AUM and pay their bills unless they have 50 stocks in their portfolio — again, you are optimizing for your happiness. This is perhaps not how other investors see their investment strategy, but try this. Ask yourself “why” repeatedly about why you do things a certain way, and you likely end up with a response like: “Because it makes me happy.”

On a related note, since I started my portfolio in 2014, I have been long-only and avoided leverage, options, and short-selling. I’m sure some type of financial alchemy could enhance my returns, but I feel more comfortable and sleep better with a buy-and-hold strategy, as outdated as it might seem.

CAGR = Compounded Annual Growth Rate

- The S&P500 data can be found here and does not use a dollar-weighted approach.

- The MSCI All Country World Index data can be found here and does not use a dollar-weighted approach.

- My returns have been calculated by Sharesight using the dollar-weighted approach and can be found here.

STIG BRODERSEN’S PORTFOLIO AS OF 31 DECEMBER 2024

Below, I have listed my current holdings. Since our founding in 2014, we have hosted a mastermind discussion roughly once a quarter where we document what we invest in and what is on our watchlist. If you’re curious about the bull theses on my positions, I’ve linked them to the corresponding mastermind discussion or other relevant episodes.

Bitcoin | Pabrai Funds | Betsson | Berkshire Hathaway | Xtracker World Value

Vanguard FTSE Emerging Markets | Physical Gold | Evolution | Alphabet | Spotify

A Few Thoughts on Bitcoin and Benchmarking

I’ve been asked why I compared my returns to a stock market index when I didn’t exclusively have stocks in my portfolio. That is such a great question, and to my point above, what I want to achieve is my financial goals. Whether I beat the S&P 500 or not doesn’t make much difference.

I also couldn’t help but wonder whether the question hinted at something along the lines of: “You cheated because you invested in Bitcoin and not only in stocks.” If so, I surely didn’t fault them for the implication. When I co-founded The Investor’s Podcast Network in 2014, I had a hard time understanding why anyone would invest in other asset classes than stocks. However, with time, I have become more pragmatic. Today, I want to get the best possible return with the least amount of risk, and it matters less whether that is achieved only with stocks. If I could get a 100% return without risk by putting my money into coffee futures or Brazilian treasuries, I would!

I invest in a specific publicly traded asset when my analysis tells me that it’s where I get the best risk-adjusted return. Sometimes I’m right, and other times I’m wrong. If it’s “cheating” to invest in a public asset that everyone can invest in, I’ll still take the higher returns any day! A dollar is a dollar… is a dollar. I don’t invest in Bitcoin for ideological reasons or because I think it will be the world’s reserve currency. At the right price, I will buy and sell, just as I would for any publicly traded stock.

While my portfolio return would take a hit from not being invested in Bitcoin, my stock market returns would certainly be better. Why? I added to my Bitcoin holdings during the COVID lows on March 29, 2020, at $5,900 per coin, six days after the S&P 500 bottomed. If I hadn’t plowed all my available cash into Bitcoin, I would have invested in individual stocks when they were on sale and captured a correspondingly higher stock return. The game of investing is a game of opportunity costs, and the stock market is no different.

Since 2014, for equities, I had a CAGR of 19.0% vs. 13.4% for the S&P500 with reinvested dividends. As mentioned above, those returns would have been better if I hadn’t invested in hard money, but my total portfolio return would have been correspondingly worse.

In my 2023 letter, I elaborated more on why I benchmarked against the MSCI World All-Country Index. I still think it’s the most appropriate benchmark, but I wanted to add the S&P 500. At first, including the S&P 500 sounds counterintuitive. I only have two US-listed stocks in my portfolio, Berkshire Hathaway and Alphabet. For the latter, the majority of its revenue is outside of the US. Another holding VFEA specifically focuses on emerging markets, and hard money, by definition, doesn’t belong in any country. With that in mind and my investments in Betsson and Evolution listed in Sweden, you could argue that it would be equally justified and arbitrary to benchmark against the Swedish stock index. So why benchmark myself against the S&P 500?

Whereas the hosts of The Investor’s Podcast Network hope to become good investors, not everyone should follow our advice. Chances are that I will underperform the stock market over the next 11 years, suggesting the previous 11 years have been pure luck.

Rather, we want to interview great investors who can educate and serve the value investing community. Therefore, when someone applies to be a guest on our shows, we ask them to send their audited track record and compare it to the S&P 500 over the past decade. You would be surprised to learn how few takers we have! Some even compose their own benchmark to find a way to “outperform.” I simply included the S&P 500 as a benchmark because it’s a common yardstick that investors can relate to and because it’s important for any organization to lead by example.

Warmly,

Stig Brodersen | 25 January 2025

The Investor’s Podcast was founded in 2014, and I have been repeatedly encouraged to publish my track record. With hesitation, I decided to disclose it for the first time in public.

The foundation of TIP has always been to provide our audience with the tools to make their own investment decisions. It has put me in a difficult situation without good solutions. Imagine the situation where I beat the market. In that case, I would run the risk of many people following my investments without doing their due diligence. I’ve seen this happen repeatedly with the herd, uncritically following certain well-known investors. In my early years, you could have counted me as a part of them, typically with a terrible result.

Disclosing a market-outperforming track record could give me certain biases, too, where I would take additional risks and make bad decisions to “beat the market.” Today, my strategy focuses more on capital preservation and less on growing the capital base. I, for example, own gold. I make no illusion that gold will outperform stocks, and I could easily paint myself into a corner where I would sell my gold holding in the quest for higher returns. In reality, I own gold as insurance in the event of – you know what – hitting the fan geopolitically and not beating a somewhat arbitrary benchmark.

Disclosing a market-outperforming track record could give me certain biases, too, where I would take additional risks and make bad decisions to “beat the market.” Today, my strategy focuses more on capital preservation and less on growing the capital base. I, for example, own gold. I make no illusion that gold will outperform stocks, and I could easily paint myself into a corner where I would sell my gold holding in the quest for higher returns. In reality, I own gold as insurance in the event of – you know what – hitting the fan geopolitically and not beating a somewhat arbitrary benchmark.

Let’s turn the tables and imagine the other scenario where I, after a decade, did not beat the MSCI All Country World Index. One could quickly conclude that I shouldn’t host a show about stock investing. After all, why listen to me when you can just buy an ETF? While it’s certainly a valid opinion, it would defeat the purpose of what we want to achieve with TIP. The hosts of We Study Billionaires do not intend to have their positions copied. Rather, we interview and study the best investors and learn alongside our audience.

My returns from 1 January 2014 to 29 February 2024 are 21.4% CAGR. The MSCI All Country World Index returned 8.9% CAGR over the same period. I calculated my returns by importing all my trades since 2014 into Sharesight. This is the methodology behind the calculation, and I’ve chosen to use the “compounded method” as this is the most conservative and is preferred to compare returns for private investors as they can control the money inflow and outflows.

It makes me humble to look back at the past 10 years, which is a very short time period for investing. With a very high level of certainty, I expect to achieve a significantly less impressive track record over the next 10 years. A track record of 20% for decades is reserved for the likes of Warren Buffett, and while you can say many things about me, being even remotely as skilled as Buffett is certainly not one of them.

It makes me humble to look back at the past 10 years, which is a very short time period for investing. With a very high level of certainty, I expect to achieve a significantly less impressive track record over the next 10 years. A track record of 20% for decades is reserved for the likes of Warren Buffett, and while you can say many things about me, being even remotely as skilled as Buffett is certainly not one of them.

Speaking about billionaires, I highly recommend reading Jeff Bezos’s wonderful book “Invent and Wander.” In a letter to his shareholders, he said (and I’m going to paraphrase) that he and the Amazon team are not much smarter because the stock price is on a tear, but also not the opposite if the stock takes a nose dive. I couldn’t agree more, as much of this is noise, and it’s no different in my case.

For example, I have been lucky to contribute more money in the most bullish years and contribute less in other years. You can see this below when you compare the results of being money-weighted and not being so. As I generally like to be fully invested, there is an element of luck when I coincidently had more new cash to invest when the “timing was right.” Though I carefully consider when to invest and at the right price, I’m well aware that it’s “time in the market” and not “timing the market” that makes you wealthy, and I expect my good luck to even out sooner rather than later.

Below, I have listed my track record compared to the MSCI All Country World Index. You’ll see the discrepancy in CAGR to be even more significant because it is dollar-weighted. In other words, as I have been very lucky to invest at the “right time” when I had better returns, and as you, by definition, can’t rely on luck, I expect much lower returns in the future. Not only did I not invest much in 2015, 2018, and 2022, which were losing years, but I proportionally had a higher inflow of capital that was put to work in the best years, such as 2017, 2020, and 2023.

I, of course, like all other investors, could be investing in non-listed assets. In my situation, I have mainly invested in private equity and my operating company, which everything else is more appealing when I can’t find alternatives in the public markets and vice versa. One could argue that my ability to “time the market” was a derivative of those opportunity costs and attributed it to skill. However, looking back, I would argue that my investment timing has overwhelmingly been due to luck. Bad decision-making in life, business, and investing has convinced me to be humble, and reviewing my surprisingly good track record doesn’t change that.

CAGR = Compounded Annual Growth Rate

STIG BRODERSEN’S PORTFOLIO AS OF 29 FEBRUARY 2024

Below, I have listed my current holdings. Since our founding in 2014, we have hosted a mastermind discussion roughly once a quarter where we document what we invest in and what is on our watchlist. If you’re curious about the bull theses on my positions, I’ve linked them to the corresponding mastermind discussion or other relevant episodes.

Bitcoin | Pabrai Funds | Berkshire Hathaway | Physical Gold | Xtracker World Value and Vanguard FTSE Emerging Markets

Alphabet | Alibaba | Teqnion | Spotify

One investment I made in 2022 that I would like to highlight is Pabrai Funds – which today is a sizable position of mine. I was torn about whether or not I should have included this in my overall return. I decided to do so because since 2014, I have interviewed hundreds of investors, and Mohnish Pabrai was the only investor I would invest with. This is an investment decision, even though you can argue that I didn’t pick the stock but the manager. In this case, I don’t see this to be too different than investing in Berkshire Hathaway stock and having Warren Buffett manage my assets.

Another thing I would like to highlight is that my private equity investments are not included in my portfolio above, as it would inflate my returns significantly. One example is a private equity investment where the General Partner wanted me to be among their investors because he felt I could add value aside from my investment in dollars. As a result, my returns went 10x the second I signed the dotted line. You can, therefore, argue that my 21.4% CAGR is on the conservative side. On the other hand, private investments often come with sweat equity that counters some of that return.

Thank you for reading to the bottom of this blog post. I wish you the best of luck with your investments.

Warmly,

Stig Brodersen | 29 February 2024